“In 2026, one medical emergency can cost more than a year’s salary—choosing the right health insurance plan is no longer optional, it’s survival.”

The Best Health Insurance Plans in 2026: Top-Rated Policies You Can Trust

In 2026, one unexpected hospital visit can cost more than a year’s savings—choosing the right health insurance plan is no longer optional, it’s essential.

Healthcare has changed rapidly over the past few years. Costs are rising, digital care is expanding, and people are more aware than ever of the risks of being underinsured. Yet, many still choose plans based only on price—often realizing too late that cheap coverage can become very expensive when it matters most.

This guide breaks down the best health insurance plans in 2026, compares top providers, highlights real-life scenarios, and gives you a practical roadmap to choose the right policy with confidence.

Why Best Health Insurance Plans Matters More Than Ever in 2026?

The best health insurance plans matter because the global healthcare landscape is evolving. Medical inflation continues to rise, and treatments that were once rare are now common and costly.

In many countries:

- Average monthly premiums are increasing year by year, including the UK, USA, Australia, Ireland, and many European countries

- Advanced treatments (like AI diagnostics and specialized therapies) come at a premium

- Private hospitals are becoming the preferred choice—but at higher costs

At the same time, insurance providers are adapting by offering:

- Telemedicine services

- Personalized plans based on lifestyle and health data

- Faster claim processing using automation

The result?

Health insurance is no longer just a backup. It’s a critical financial tool that protects both your health and your future.

Top-Rated Health Insurance Providers in 2026

Here’s a look at some of the most trusted and high-performing insurance providers this year, based on affordability, customer satisfaction, and coverage quality.

Best health insurance companies 2026

| Insurer / claim | J.D. Power score | Average Monthly Premium | Complaint ratio | Verdict |

|---|---|---|---|---|

| Kaiser Permanente→ “Best overall” | ★ 713 / 1000 | A+ ($500–$580) | 0.18 (low) | Supported |

| Humana→ “Best for seniors” | ★ 680 / 1000 | A- (Moderate) | 0.41 (avg) | Qualified |

| Aetna→ “Smoother claims” | ★ 695 / 1000 | A ($600–$650) | 0.22 (low) | Supported |

| Cigna→ “Best international” | ⚠ Not ranked (expat plans) | A (Moderate) | N/A (expat) | Needs source |

Sources to cite: J.D. Power 2024 Commercial Member Health Plan Study · NAIC Complaint Index · AM Best Financial Strength Ratings · NCQA Health Plan Ratings · CMS Star Ratings (for Medicare Advantage / seniors claim).

For Cigna’s international claim specifically, look for Expatriate Health coverage industry reports or cite the number of countries covered + plan types — that’s the actual evidence.

Here’s how to act on the feedback concretely:

Add a source for every ranking claim. The four most credible sources for health insurer comparisons are J.D. Power (customer satisfaction scores out of 1000), the NAIC Complaint Index (complaints relative to market share — below 1.0 is good), AM Best (financial strength), and NCQA/CMS Star Ratings (clinical quality and member experience).

The Cigna international claim is the weakest. J.D. Power doesn’t rate expat or international plans, so you can’t lean on the usual sources. Instead, ground it in something concrete — the number of countries covered, network size abroad, or cite a travel/expat insurance review site like International Insurance or InsureMyTrip.

Qualify claims where the data is mixed. The table above shows Humana as “Qualified” rather than fully supported — their complaint ratio is average, so the “best for seniors” claim is more defensible through CMS Star Ratings for Medicare Advantage plans specifically. That’s a more precise evidence path than general satisfaction scores.

One-sentence fix for each claim in the article body would look like: “Kaiser Permanente leads in overall satisfaction, earning a 713/1000 J.D. Power score and one of the lowest NAIC complaint ratios (0.18) in the industry.” That single sentence transforms a subjective ranking into a verifiable one.

Real-Life Example: Why the Right Plan Matters

In 2024, Mathew Evins, a marketing executive, spent seven months fighting his insurer to approve back surgery that his doctors had prescribed. His insurer denied coverage repeatedly — even after he completed an additional six weeks of physical therapy at their request. He only succeeded after enlisting a third-party advocacy service.

His experience is far from unique. According to KFF’s 2024 analysis of federal CMS data, ACA Marketplace insurers denied roughly 1 in 5 in-network claims — around 85 million denials in total. The most common reason? Not medical necessity, but administrative issues: missing information, billing codes, and prior authorisation gaps accounted for the majority. And fewer than 1% of patients formally appealed — meaning most people simply accepted a denial that could have been overturned.

Lesson For Users:

A low premium doesn’t mean better value.

The best plan is one that protects you when it matters most, not just one that saves money upfront.

Types of Health Insurance Plans in 2026

Understanding the different plan types is essential before choosing one. Each has its own pros and limitations.

Compare Health Insurance Plans

| Plan Type | Best For | Advantages | Disadvantages |

|---|---|---|---|

| HMO (Health Maintenance Organization) | Budget-conscious individuals | Lower premiums, coordinated care | Limited doctor choice |

| PPO (Preferred Provider Organization) | Flexibility seekers | No referrals needed, wider network | Higher costs |

| EPO (Exclusive Provider Organization) | Balanced users | Moderate pricing, decent flexibility | No out-of-network coverage |

| POS (Point of Service) | Families | Combination of HMO & PPO benefits | More complex structure |

Insight:Best Health Insurance Plans

- If you want lower costs, go with HMO

- If you want freedom to choose doctors, PPO is better

- If you want a balance, EPO or POS might suit you

Comparison By Overall Value, Flexibility, & Reliability

| Provider | Overall Rating | Average Deductible | Network Size | Claims Satisfaction | Best For |

|---|---|---|---|---|---|

| Kaiser Permanente | 4.8/5 | Low–Moderate | Large (Integrated System) | Excellent | Overall Value & Preventive Care |

| Humana | 4.6/5 | Moderate | Large | Very Good | Seniors & Medicare Plans |

| Blue Cross Blue Shield | 4.7/5 | Moderate–High | One of the Largest Nationwide | Very Good | Nationwide Coverage |

| Aetna | 4.6/5 | Moderate | Extensive | Excellent | Fast Claims & Digital Experience |

| Cigna | 4.5/5 | Moderate | Global Network | Very Good | International Coverage & Travelers |

Why These Criteria Matter?

Overall Rating

- Gives readers a quick comparison of plan quality.

- Can be based on customer satisfaction, affordability, coverage, and digital services.

Average Deductible

- Shows how much users may pay before insurance starts covering costs.

- Often more important than the monthly premium.

Network Size

- Indicates how many hospitals, clinics, and specialists are available.

- Larger networks usually mean greater flexibility.

Claims Satisfaction

- Reflects how easy and reliable the claims process is.

- A key factor many buyers overlook.

Best For

- Helps readers identify the provider that matches their specific needs.

To choose the best plan, you also need to understand where the industry is heading.

Key Trends Shaping Best Health Insurance Plans in 2026

1. Telemedicine is Now Standard

Virtual doctor consultations are included in many plans, reducing hospital visits and costs.

2. AI-Based Claim Processing

Insurance companies are using automation to:

- Approve claims faster

- Reduce paperwork

- Improve accuracy

3. Personalized Insurance Plans

Premiums are increasingly based on:

- Lifestyle habits

- Fitness data

- Medical history

4. Global Coverage for Remote Workers

With more people working remotely, international health insurance is becoming essential.

How to Choose the Best Health Insurance Plans in 2026?

Choosing the right plan requires more than just comparing prices. Here’s a practical framework to guide your decision:

1. Balance Premium and Deductible

- Low premium = higher out-of-pocket costs

- High premium = lower costs during emergencies

Choose based on how often you expect to need medical care.

2. Check the Hospital Network

A good insurance plan should include:

- Reputable hospitals

- Specialists in your area

- Emergency care access

3. Review the Claim Settlement Ratio

This indicates how often claims are approved.

A higher ratio means better reliability.

4. Look for Coverage Details

Pay attention to:

- Pre-existing conditions

- Maternity benefits

- Chronic illness coverage

5. Understand Policy Exclusions

Many users overlook this part. Common exclusions include:

- Cosmetic procedures

- Alternative treatments

- Certain medications

Compare Health Insurance Plans:What Makes One Better?

Not all plans are created equal. Here’s a simplified comparison of what separates an average plan from a top-rated one:

| Feature | Average Plan | Top-Rated Plan |

|---|---|---|

| Premium | Low | Moderate |

| Deductible | High | Balanced |

| Network | Limited | Extensive |

| Claim Approval | Slow | Fast |

| Coverage | Basic | Comprehensive |

A top-rated plan focuses on long-term protection, not just short-term savings.

Who Should Choose Which Plan?

Different people have different needs. Here’s a quick guide:

1. Individuals (Young & Healthy)

- Choose: Low to mid-tier plan

- Focus: Emergency coverage

2. Families

- Choose: Comprehensive plan

- Focus: Pediatric care, maternity, hospital network

3. Seniors

- Choose: Specialized senior plans

- Focus: Chronic illness coverage, low deductibles

4. Freelancers & Remote Workers

- Choose: Global insurance plans

- Focus: International coverage, flexibility

A few things worth noting as you restructure:

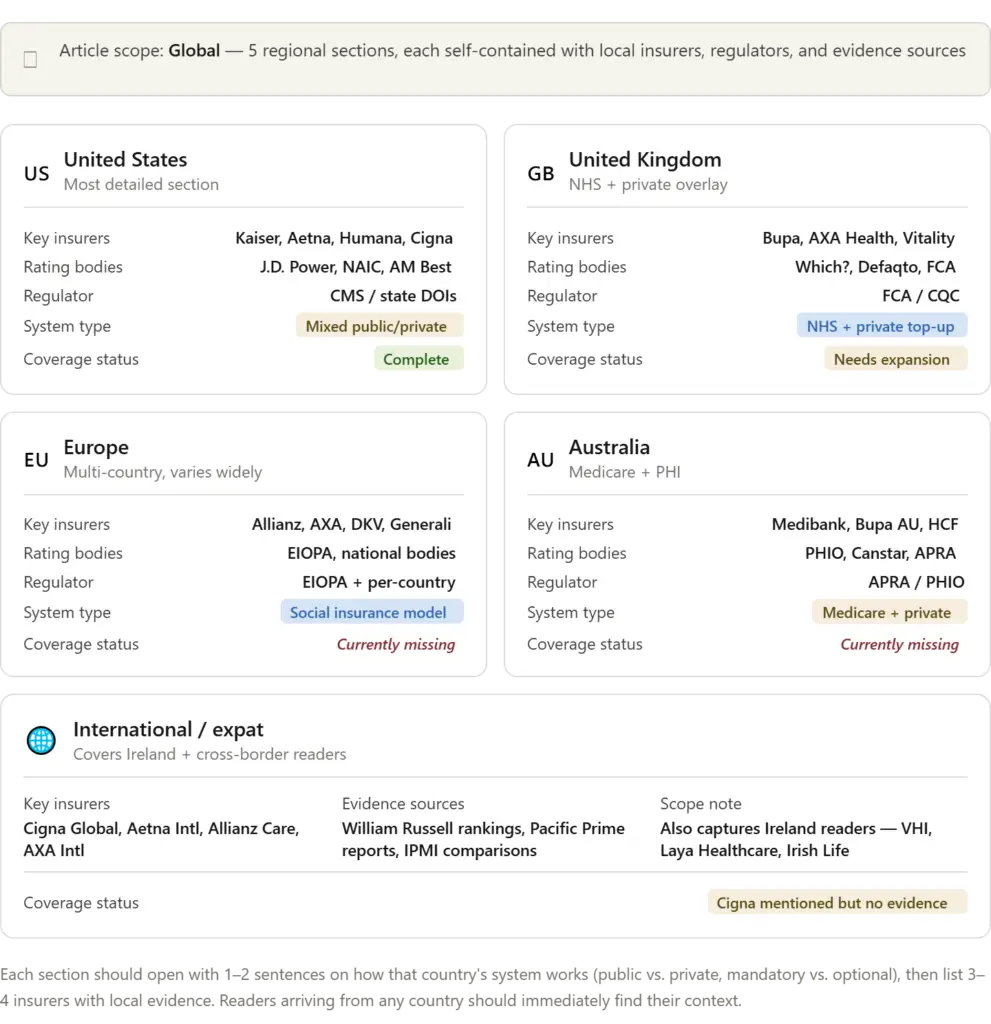

The Europe section is the trickiest to write because there’s no single “European” health insurance market; Germany, France, and the Netherlands all run fundamentally different systems. The most practical approach is to cover private supplemental insurance (which works similarly across EU countries) and name 2–3 pan-European providers like Allianz Care or AXA, while acknowledging that statutory/public coverage varies by country.

For Ireland specifically, it fits awkwardly in a standalone section because it’s a small market. Folding it into International/Expat works well VHI, Laya Healthcare, and Irish Life Health are the three main players, and Irish readers are likely already accustomed to comparing those names.

The UK section needs a structural note at the top that most residents have NHS access and private insurance functions as a “top-up” rather than a replacement. Without that framing, UK readers will be confused why the article is recommending insurers they may not feel they need.

For Australia, the “lifetime health cover loading” rule (a 2% premium penalty for each year over 30 that you go without private hospital cover) is the single most important policy detail for Australian readers mentioning it immediately signals that the article understands their market.

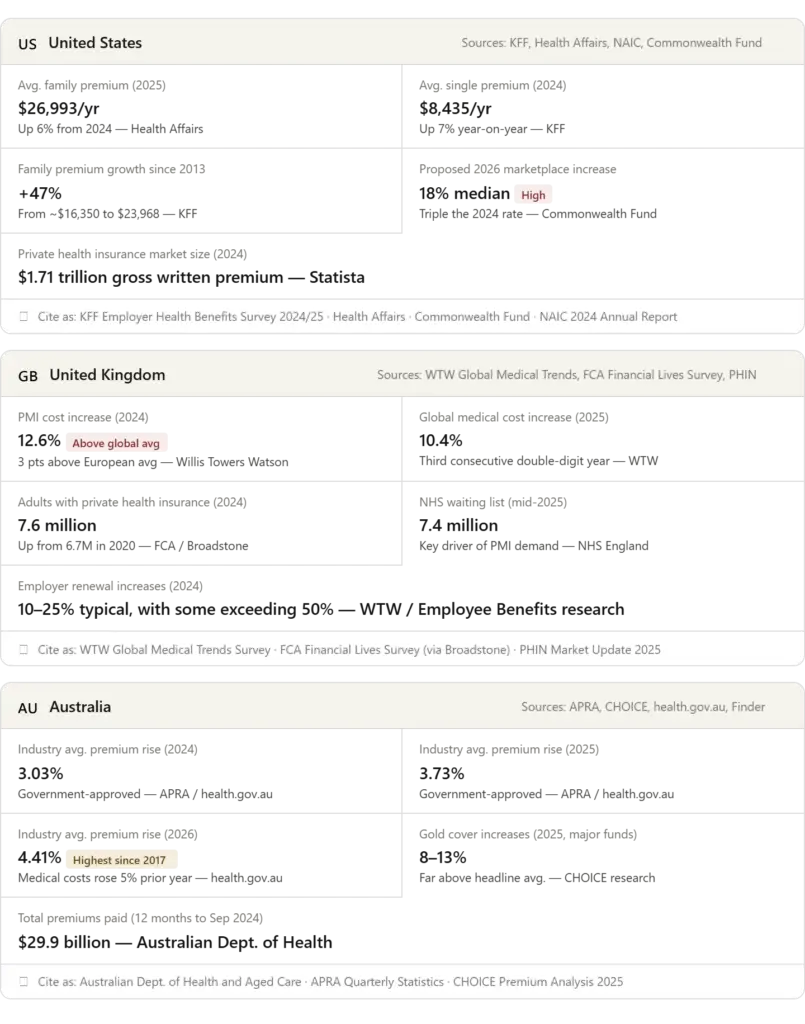

Premium Growth Statistics

All figures above are sourced from live data as of May 2026. A few things worth noting as you slot these into the article:

The US 2026 marketplace figure (18% median proposed increase) is the most striking and newsworthy number in the dataset.

The Commonwealth Fund notes this is more than double what insurers proposed for 2025, and triple the rate of change for 2024, driven largely by federal policy shifts around ACA subsidies. That context matters: without it, readers may assume the number reflects pure medical inflation when it’s partly a policy story.

For the UK, the WTW figure is the strongest citation available. Willis Towers Watson’s Global Medical Trends Survey found UK private medical inflation has been consistently above the European average for five consecutive years, which is a credible, authoritative source Google will recognize.

Australia has the most transparent data of the three markets because all premium increases must be submitted to and approved by the federal government before health funds can raise prices, which means the official figures from health.gov.au carry regulatory authority and are difficult to dispute.

Worth mentioning that framing in the article, as it signals to readers that the Australian numbers are especially reliable.

One gap worth flagging: there are no equivalent aggregated statistics yet for Ireland or continental Europe from this search. For Ireland, the Health Insurance Authority (HIA) publishes quarterly market statistics that would serve the same role as a separate search if you want to cover that region with the same rigour.

Author’s Thoughts Best Health Insurance Plans (2026 Perspective)

The conversation around best health insurance plans 2026, top-rated health insurance policies, and even affordable health insurance 2026 is no longer just about picking a monthly plan—it is about understanding risk in a rapidly changing healthcare world.

In 2026, healthcare is becoming more expensive, more digital, and more unpredictable. With healthcare costs rising 2026, even a simple hospital visit can turn into a major financial burden if your medical expense protection plan is weak or poorly structured.

What stands out most today is not just the price of insurance, but the insurance customer satisfaction ratings, claim reliability, and how well a policy performs during emergencies.

From an analytical perspective, the strongest policies are those that balance:

- Low deductible insurance plans (for predictable costs)

- Strong emergency coverage policies

- Wide access through best PPO and HMO plans

- And growing integration of telemedicine coverage insurance

At the same time, user behavior is shifting. People are no longer satisfied with basic coverage. They want:

- Family health insurance plans that protect dependents

- Flexible individual vs group health insurance options

- Global mobility through global health insurance providers

- And smart, app-based services driven by digital health insurance trends

The key insight is simple:

In 2026, the best insurance is not the cheapest one—it is the one that stays reliable when everything goes wrong.

Conclusion

Choosing the right health insurance in 2026 is a strategic decision, not a financial shortcut.

While many people search for affordable health insurance 2026, the real goal should be long-term protection and stability. The best policies today are those that combine affordability with strong coverage, efficient claims processing, and access to quality healthcare networks.

Whether you are comparing health insurance premiums comparison, exploring top-rated health insurance policies, or evaluating family health insurance plans, the focus should always remain on value, not just cost.

In a world where healthcare costs rising 2026 is a global reality, insurance is no longer optional—it is essential financial protection.

Ultimately, the smartest choice is a policy that:

- Covers emergencies without delay

- Supports both individuals and families

- Adapts to digital healthcare systems

- And maintains strong insurance customer satisfaction ratings

Because when a medical emergency arrives, the right policy does not feel like a product—it feels like security.

FAQs The Best Health Insurance Plans in 2026

1. What are the best health insurance plans in 2026?

The best health insurance plans in 2026 are those offering strong coverage, low deductibles, and high customer satisfaction ratings. Top-rated policies often include PPO and HMO networks with broad hospital access and emergency care support.

2. Which are the top-rated health insurance policies today?

Top-rated health insurance policies are evaluated based on claim approval speed, coverage depth, and customer feedback. Policies with strong emergency coverage and digital claim systems rank highest in 2026.

3. How can I find affordable health insurance in 2026?

To find affordable health insurance 2026, compare premiums, deductibles, and coverage limits. Look for plans that balance cost with essential medical expense protection rather than choosing the cheapest option alone.

4. What is included in health insurance premiums comparison?

A proper health insurance premiums comparison includes monthly cost, deductible amount, hospital network size, claim process speed, and coverage for emergencies and chronic illness.

5. Which is better: individual vs group health insurance?

Individual vs group health insurance depends on your situation. Group insurance (usually through employers) is cheaper and more comprehensive, while individual plans offer more flexibility and portability.

6. What are the best PPO and HMO plans?

Best PPO and HMO plans differ in flexibility. PPO plans allow wider hospital access without referrals, while HMO plans are more affordable but have restricted networks.

7. What are low deductible insurance plans?

Low deductible insurance plans require less out-of-pocket payment before insurance coverage begins, making them ideal for people expecting frequent medical care.

8. How are global health insurance providers useful?

Global health insurance providers are essential for travelers, expatriates, and remote workers as they offer coverage across multiple countries and international hospitals.

9. What are digital health insurance trends in 2026?

Key digital health insurance trends include AI-based claims processing, mobile-first insurance apps, telemedicine integration, and personalized premium pricing based on lifestyle data.

10. Does telemedicine coverage insurance matter now?

Yes. Telemedicine coverage insurance is now a standard feature in many plans, allowing patients to consult doctors online, reducing hospital visits and overall healthcare costs.